A Rebound in Bond Performance

Baird Trust's John Craddock weighs in on recent bond market performance and what to expect from the Fed in an election year.

2023 ended with some welcome performance from the bond market.

In our October newsletter, we mused that 2023 could be yet another year of negative returns for the fixed income market. But instead of “three in a row,” we witnessed a significant market rally during the final months of the year, and 2023 returns for intermediate bonds were solidly positive. In fact, investment grade bonds returned more than 5% – and in many cases closer to 6% – for the full calendar year.

For much of last year, money market inflows were large by historical standards, and there was evidence of significant cash on the sidelines and heavy investments in short-term Treasury bills. In the fourth quarter, however, investors turned positive on the 5+% yields offered by intermediate-term bonds, and significant amounts of cash entered the bond market. This sudden increase in demand provided a technical tailwind that has continued into 2024.

Baird Trust bond portfolios were positioned with an overweight in investment-grade corporate and high-quality municipal bonds for most of 2023, allowing our investors to earn higher yields for the entire year. Overweight positioning in corporate bonds – especially in the banking and industrial segments – was the primary driver of outperformance across accounts. Exposure to callable agency bonds issued by Aaa-rated Federal Home Loan Bank and Federal Farm Credit Bank also helped. Early in 2023, most Baird Trust portfolios were positioned slightly short of benchmark with respect to average maturity and duration. This short position was returned to a more neutral stance during the summer, which ultimately added value as rates fell into year-end.

Four months into 2024, it is important to note that the yield advantage of corporate bonds versus Treasury bonds has fallen to levels we last experienced in 2021. As a result, corporate bonds are somewhat less attractive than they were just a few months ago, and our recent additions have tilted toward Treasury and agency bonds to take advantage of any opportunities that might arise later this year. In any case, at the close of the first quarter, intermediate-term bonds are still hovering around the 5% yield level, which bodes well for continued positive bond returns in the coming years.

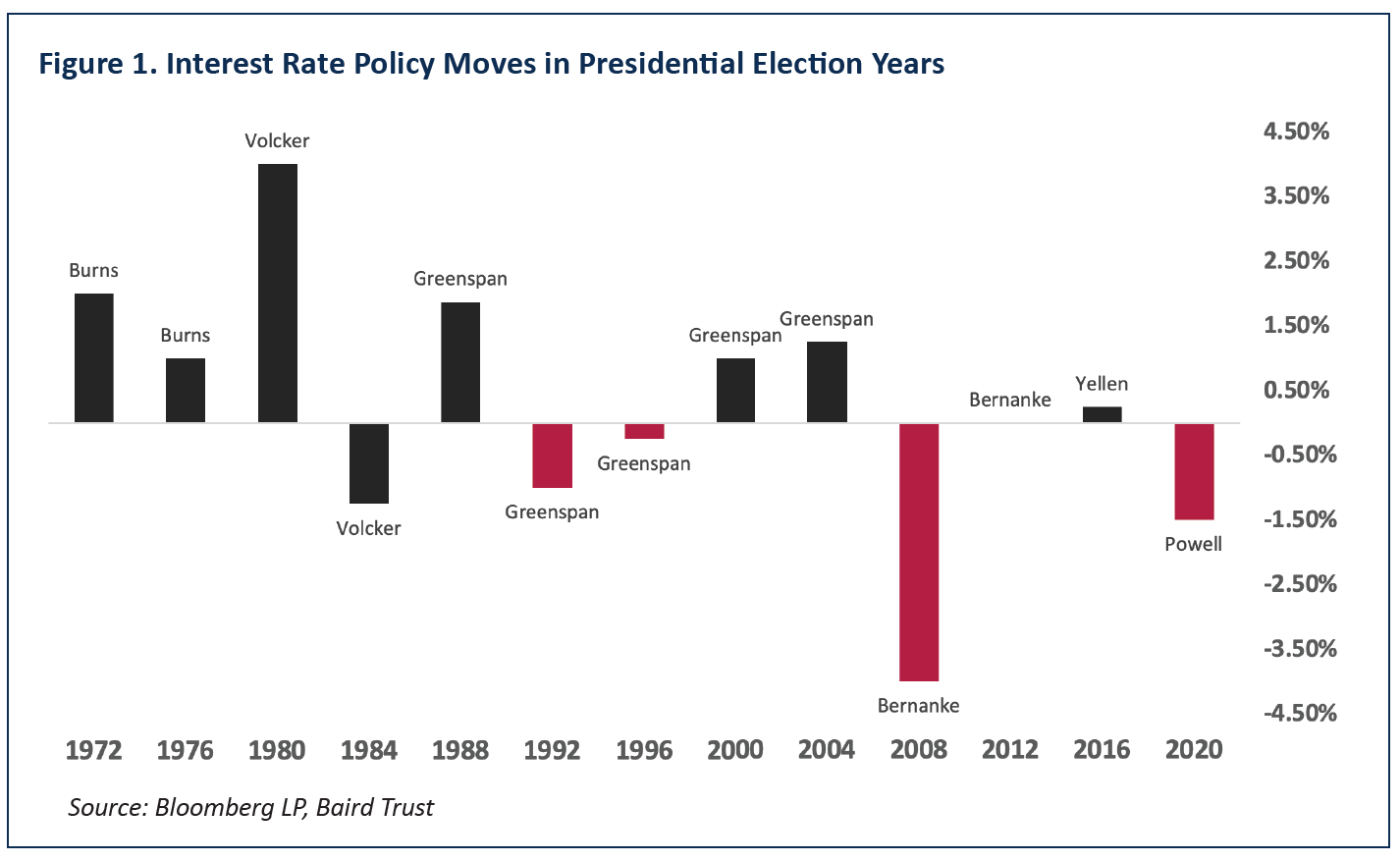

Presidential Election Years and Federal Reserve Policy

With 2024 being a presidential election year, there is a lot of talk about how politics might affect U.S. interest rate policy. We believe that the economy, rather than politics, is the primary driver of monetary policy, and that the outcome of November’s election might not have as great an impact on longer-term bond investors as some market watchers expect. One area we’re particularly focused on is the potential for rate cuts.

You might recall the Federal Reserve raised overnight rates from zero in early 2022 to over 5.25% by the middle of 2023 in its fight against inflation. The Fed is now signaling that rate cuts might come sometime this year – but the question is when. Higher-than-expected inflation readings and strong employment readings have pushed back rate cut expectations, and the Consumer Price Index and Personal Consumption Expenditures Index have similarly shown that goods and services prices are moderating slower than expected. If economic data continues to print on the “strong” side, it’s possible the Fed could push the first rate cut into the fall – right in the middle of the presidential election.

The Federal Reserve might choose to begin policy actions over the summer to avoid a perception that they are trying to influence voters. But one thing is for certain: As the following chart shows, the Fed has plenty of precedent for adjusting policy in an election year. In 2004, then-Fed Chair Alan Greenspan started a hiking cycle at the June meeting of that year and proceeded to hike rates in quarter-point increments at every remaining meeting that year, including those immediately before and after the November presidential election. The Fed didn’t hesitate to cut rates in both 2008 and 2020, both times in the face of quickly deteriorating markets.

Meanwhile, the Fed is often subject to enormous pressure from politicians. In January 2024, Senator Elizabeth Warren, with the support of Democratic colleagues, wrote a letter to Fed Chair Jerome Powell imploring the Fed to lower “these astronomical rates.” Donald Trump said in early February that he would not reappoint Powell, whose term ends in 2026, saying, “I think he’s going to do something to probably help the Democrats, you know, I think if he lowers interest rates.”

Thankfully, the Fed seems to have an unwavering focus on the economic data and an ability to push electi on noise to the background. Ultimately, economic factors – and especially the upcoming inflati on readings – are going to drive decisions on rate policy, not the rhetoric of politicians. As Powell said in December, “We don’t think about politics – we think about what’s the right thing to do for the economy.”

We at Baird Trust follow a similar credo: We will focus less on the upcoming election extravaganza and more on the right things to do for your portfolio.

Baird Trust Company (“Baird Trust”), a Kentucky state-chartered trust company, is owned by Baird Financial Corporation (“BFC”). It is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), an SEC-registered broker dealer and investment advisor, and other operating businesses owned by BFC. Past performance is not a predictor of future success. All investing involves the risk of loss and any security may decline in value. This is not intended as a recommendation to buy any security and views expressed may change without notice. Baird Trust does not provide tax or legal advice. This market commentary is not meant to be advice for all investors. Please consult with your Baird Financial Advisor about your own specific financial situation.