What’s in a Coupon?

As recent issuances have shown, just because a bond offers a higher coupon rate doesn’t necessarily mean it’s a better investment.

In William Shakespeare’s Romeo and Juliet, Juliet asks the question “What’s in a name?” implying names can mean very little with respect to the underlying character of each of us. In this discussion, we ask the question “What’s in a coupon?” – as in bond coupon. But first, let’s recall what a bond coupon is exactly.

Back in the “bad old days” before computers simplified financial record keeping, investors who bought bonds were given physical certi ficates with “coupons” that could be clipped off and returned for cash interest. While we no longer use physical coupons, the term “coupon” is still around to signify the amount of interest a particular bond pays out to its owner. Indeed, the rapid rise in rates over the past year has led to much larger coupons for recently issued bonds. Below we will explore how a coupon does and does not affect the return potential of individual bonds and how Baird Trust manages coupon rates within bond portfolios.

“COVID Coupons” Versus Newer, Higher Coupons

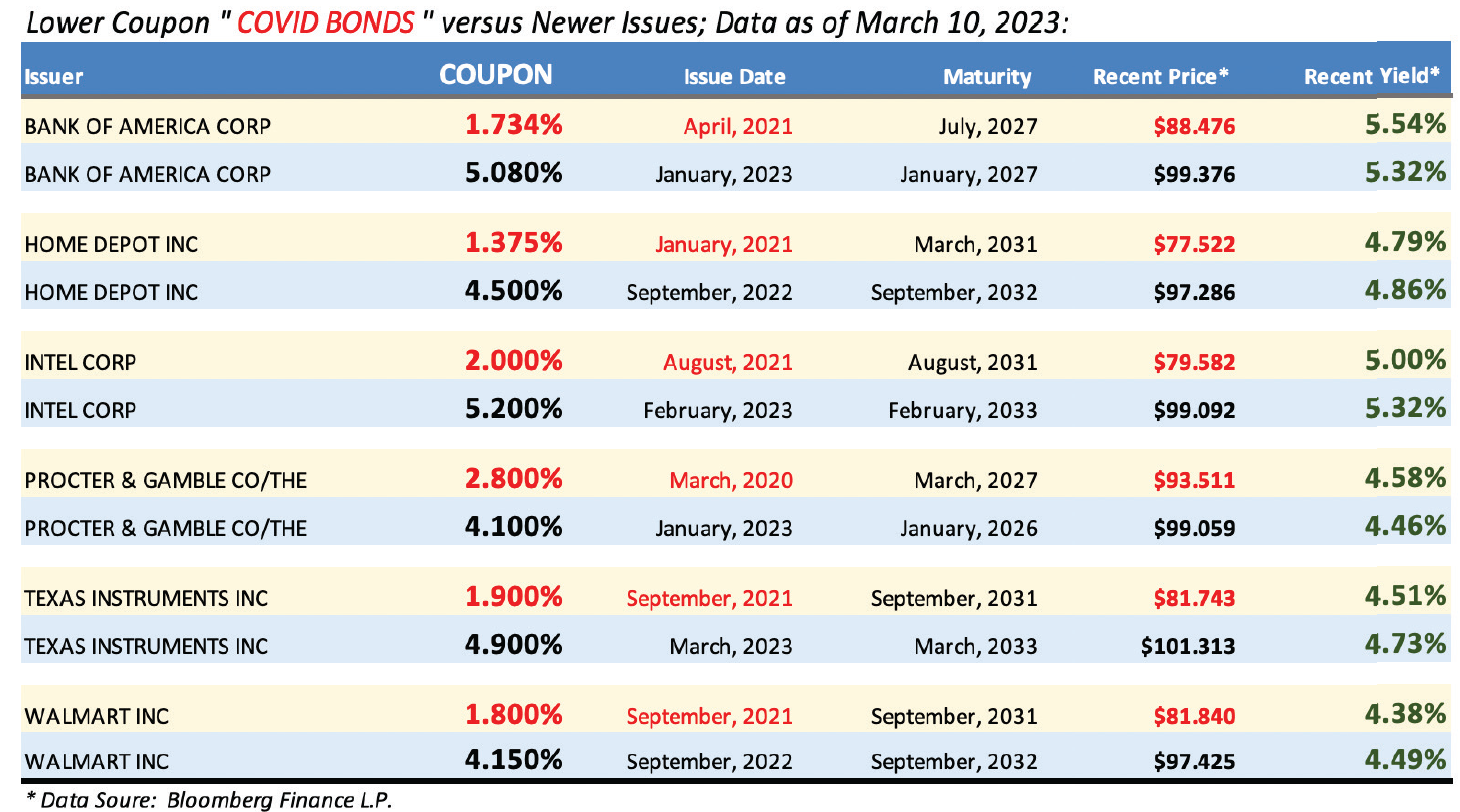

As Table 1 shows, many investment-grade issuers were able to print bonds with coupons well under 3% and sometimes even below 2% during the COVID Years of 2020 and 2021. This was a period of record-setting low interest rates, when even the popular 30-year home mortgage rate dropped below 3%. As a result, there is a long list of bonds with very low coupons now lingering in portfolios everywhere. These bonds are easily spotted in statements as they typically have dollar prices significantly below $100. In contrast, as interest rates have risen over the past several months, we have witnessed the creation of 4%, 5% and even 6% coupon bonds from the very same issuers.

The yield of a bond represents the overall earning power over its life and results from both coupon cashflows and gains (or losses) at maturity. While the relatively lower coupon bonds in the chart provide reduced near-term cashflow compared to the higher coupon bonds, the yield levels are similar. Lower coupon bonds, in effect, exchange near-term cashflow for cashflow gains at maturity. The result, as seen in the “Recent Yield” column, is that lower coupon bonds purchased at a discount will usually return just as much as higher coupon bonds over their life. Note too that the overall expected rate of return for a bond can vary significantly from the coupon rate—especially if the bond is trading at a large discount or premium price. And so while the coupon rate of a bond and its yield may seem like the same thing, they are not.

Bonds with Lower Coupons Tend to Have Lower Prices

Low coupon bonds with discount prices require a smaller principal outlay relative to par, or face value. For example, if a bond is priced at $80, purchasing $10,000 in face value will only cost $8,000. The maturity value for bonds is known, so barring a default, there is a known appreciation value at the time of purchase. The bond value will fluctuate based on market conditions, but it will “pull towards par,” moving toward the face value of the bond over time. Importantly, this appreciation is in addition to the bond’s periodic coupon payments.

U.S. Treasury Bills (T-Bills) are great examples of “low coupon” bonds—in fact, T-Bills have no coupon at all! However, this does not prevent them from providing income and positive return on investment. T-Bills are bought at a discount to par and then pay out full par value at maturity. For example, in today’s environment, you might pay $9,500 for T-Bills that pay out $10,000 par at maturity one year later. It is the difference between par value and the discount price paid that results in income—no coupon was required in this case. This is a prime example of where coupon does not determine yield or earning power.

Investors who are looking to fund a future liability, such as purchasing a home or dream car or perhaps funding a grandchild’s college tuition, might in fact prefer low coupon bonds. In these cases, current income is not a priority and the lower price of a low coupon bond reduces the required cash outlay for a given cashflow at maturity.

When Does Coupon Matter?

While a bond’s coupon by itself does not determine yield or its price, the coupon does influence near-term cashflow amounts to the investor, the premium or discount price level, and to some extent the interest rate sensitivity of the bond.

The main attribute that coupon rate controls is the amount of current cash income that a particular bond will return to investors. All else equal, higher coupons generate more near-term cash than lower coupon bonds. However, again all else equal, higher coupon bonds will cost more to buy and produce less accretion to par than lower coupon bonds. The total return potential of a bond cannot be determined by coupon alone—it is the combination of coupon, price, and remaining payment schedule that results in a particular yield for each bond.

Baird Trust balances the search for yield and coupon rate, considering there are advantages in having current, near-term cashflow coupled with maximum available yield for a given set of objectives and risk tolerance. Yes, it is possible to sell lower coupon bonds and buy higher coupon bonds, thereby increasing near-term cashflow, but it will come at the expense of buying fewer bonds, and paying more for them. In such a scenario, total earning power of the bond portfolio could even be reduced due to the trading costs involved in swapping bonds. Investors do well to remember that low coupon bonds are currently valued at discount prices but will continue to accrete towards $100. At maturity, the bonds will provide much more dollar value than the current “market value” shown on statements.

Keeping Cashflows Consistent

Because interest rates fluctuate over time and coupons vary in size, Baird Trust strives to keep maturities diversified for clients. Periodic maturities enable reinvestment into “current coupons” in a way that keeps cashflows consistent with market rates over time. Baird Trust also emphasizes higher-quality, large benchmark bonds that can be sold if funds are needed above and beyond coupon flows. Even selling partial par amounts is possible to provide additional near-term cashflow if needed.

If you have become envious of high coupons, it may help to focus not on the coupon rate of your bonds but on the total par amount owned; all else equal, higher coupons translate into less par value. While you could theoretically move “up in coupon,” you would simultaneously be moving down in total par amount. Quite simply, higher coupon bonds are more expensive and you can buy less of them than lower coupon bonds. And just like the name “rose” does not make the flower smell any sweeter, a high coupon rate by itself does not make the bond return any higher.

Baird Trust Company (“Baird Trust”), a Kentucky state chartered trust company, is owned by Baird Financial Corporation (“BFC”). It is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), (an SEC-registered broker dealer and investment advisor), and other operating businesses owned by BFC. Past performance is not a predictor of future success. All investing involves the risk of loss and any security may decline in value.

Fixed income is generally considered to be a more conservative investment than stocks, but bonds and other fixed income investments still carry a variety of risks such as interest rate risk, credit risk, inflation risk and liquidity risk. In a rising interest rate environment, the value of fixed income securities generally declines and conversely, in a falling interest rate environment, the value of fixed income securities generally increases. High-yield securities may be subject to heightened market, interest rate or credit risk and should not be purchased solely because of the stated yield. Municipal securities investments are not appropriate for all investors, especially those taxed at lower rates.

This is not intended as a recommendation to buy or sell any security and views expressed may change without notice. Baird Trust does not provide tax or legal advice. This market commentary is not meant to be advice for all investors. Please consult with your Baird Financial Advisor about your own specific financial situation.