In Times Like These, Remember Why You Own Bonds

It’s hard to read the news these days without breathless articles about soaring interest rates, high inflation or how the “cost of money” is climbing faster than ever. For bond investors, a general rise in interest rates – like what we’ve seen to start 2022 – is essentially a double-edged sword: While we’ve seen bond prices fall and could even see unrealized losses, we’re also able to invest current cashflows into higher-yielding securities, which sets us up for greater future returns. Even so, falling prices can give many investors pause as they assess this year’s bond performance – by some measures, the first several months of 2022 witnessed the worst bond returns to begin a year since 1980.

Is It 1980 All Over Again?

When we talk about bond returns, it is useful to reference a popular, long-established benchmark like the Bloomberg U.S. Aggregate Bond Index, commonly referred to as “the Agg.” Since the mid-1970s, the Agg has been an across-the-board flagship index that measures all types of investment-grade, U.S. dollar taxable bonds (think U.S. Treasurys, corporate bonds, mortgagebacked bonds and the like).

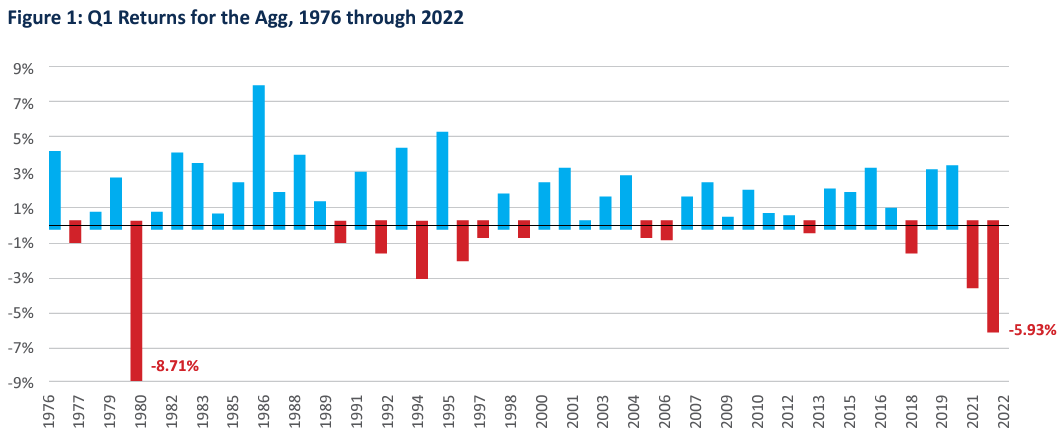

Figure 1 shows each first-quarter total return for the Agg since 1976. The long red pummeling on the left side of the chart represents bond performance in the first quarter of 1980. At that time, the 10-year Treasury yield rose to over 13%, which led to a total return of -8.71%.

Fans of the Pittsburgh Steelers and Louisiana Tech Bulldogs might remember this period for another reason. Back in early 1980, Terry Bradshaw’s Steelers were heavily favored to win Super Bowl XIV. But like the bond market that year, they found themselves trailing early in the game to a Rams team that barely had more wins than losses. For both investors and football fans, the lesson was that things don’t always go as expected.

Fast-forward 42 years, and history seems to repeat itself: During the first quarter of 2022 the Agg returned -5.93%, and just as the Steelers were trailing at halftime in the 1980 Super Bowl, through June 30, 2022, the Agg was down more than 10% – and the S&P 500 was down about 20%.

So by this measure, 2022 has represented the worst start in a year for bonds since 1980, rattling many investors who depend on their bond portfolio for stability, reliable income and an offset to stock market drops. While it’s true that making bonds a part of a diversified portfolio typically “smooths the ride” for investors over the long term, investors in this year’s markets have been reminded that this outcome is far from guaranteed.

During times like this, when both stocks and bonds fall in value and investor angst builds, it is important to keep in mind some fundamentals of how bonds are different from stocks.

Take Comfort in Coupon and Principal Cashflows

As suggested by the term “fixed income,” bonds are essentially a stream of known cashflows, typically consisting of semiannual coupons and a principal payment at maturity. Investors should remember that these cashflows are not affected by the price movement of the bond, and that issuers do not have the option to skip or defer payments as they do, for instance, with stock dividends. Investors can take comfort knowing that, short of outright default, coupon payments will continue to flow despite the current price volatility.

Further, with each passing day the return of principal gets closer to reality. Unlike stocks, bonds obligate the issuer to return your principal cash to you – no sell transaction required. That is how the bond cycle works: Bonds are born, they live for a while and pay coupons, and then they mature and go to “bond heaven.” While prices may fluctuate in the short term, future cashflows, absent the unlikely event of a default, do not change – periodic coupons are being paid and full principal values are being returned at maturity. And the best part is, sometimes we get to invest these dollars at higher rates, like what 2022 has offered so far.

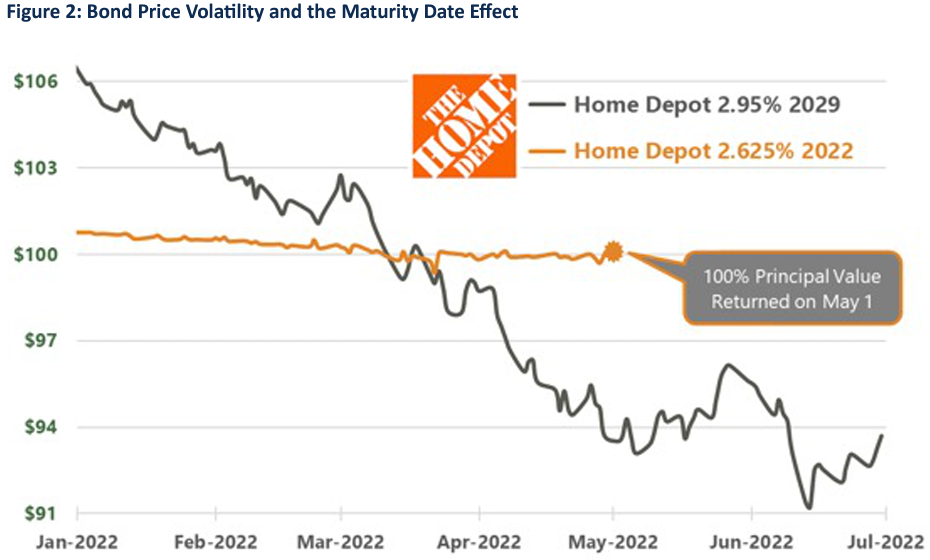

Another dynamic bond investors should be aware of is the relationship between time to maturity and price volatility. In Figure 2 we examine the recent price movement of two different bonds from the same issuer, one with a 2022 maturity and the other with a 2029 maturity. Throughout its lifecycle, the 2022 Home Depot bond paid all 14 of its coupons and returned 100% of its principal value on May 1. While the longer 2029 bond experienced significantly more price volatility earlier this year than did the 2022 bond, it too has continued to pay regular coupons and is on track for 100% principal return, just like its 2022 cousin. As an investor, take comfort in these fixed cashflows and understand that price volatility is only temporary. As it nears maturity, the 2029 Home Depot bond will become less sensitive to interest rate moves, allowing it to one day behave similarly to its 2022 cousin and find its way back to that “par value” of $100.

Time Is a Bond Investor’s Best Friend

Given the volatile rate environment we’re experiencing in 2022, never forget the steady coupon flow and “pull to par” of your bond holdings – both are friends to the bond investor. Your portfolio management team at Baird Trust works to ensure portfolios have laddered maturities, focusing on upper-tier investment-grade issuers and always having periodic cashflows to reinvest at current rates. This means that the typical Baird Trust bond portfolio is underweight or even void of bonds with 20, 30 or even 40 years to maturity like many of those found in the Agg. We believe a moderate, consistent maturity structure lies at the heart of sound bond portfolio construction.

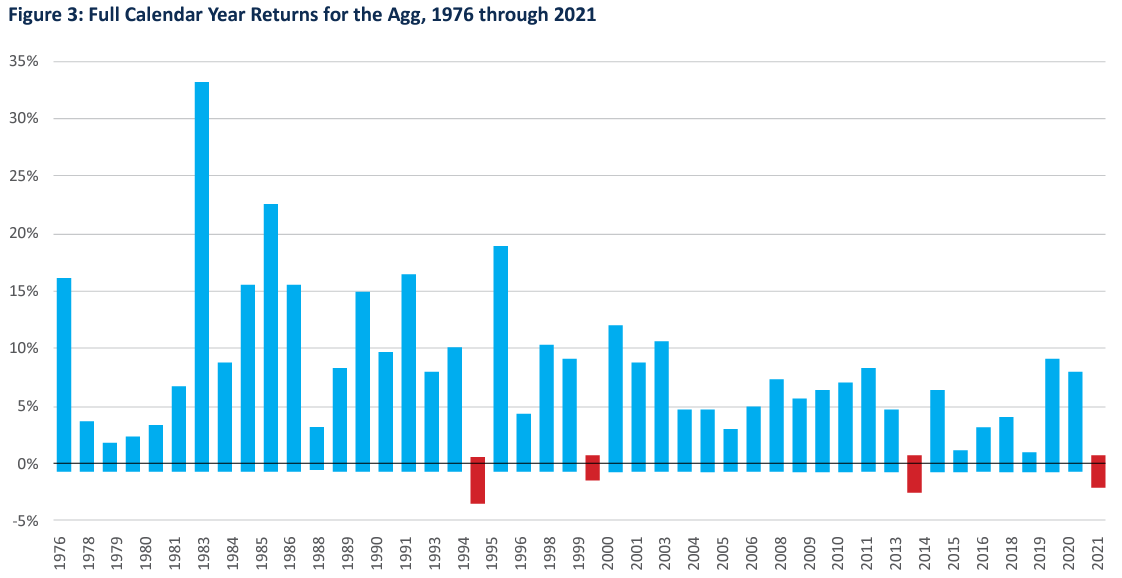

While we never welcome a “bad start” to the year, it does not have to dictate full-year returns. Figure 3 bears witness that bond returns often recover after a challenging beginning to any given year. Note that of the previous 13 negative starts for the Agg, in only four did the Agg fail to produce positive returns for the full calendar year. So if 2022 really is a 1980 replay for bonds, we may have some better news coming later this year.

If we turn one last time to the gridiron in early 1980, the normally reliable Steelers came back from that halftime deficit to take a second-half lead (thanks to a 47-yard touchdown pass from Terry Bradshaw to Lynn Swann) and ultimately win Super Bowl XIV. Similarly, despite the rough start, the Agg ended 1980 in positive return territory – up +2.71% for the full calendar year! So let’s allow time to be our friend, collect bond coupons and principal cashflows as we go, and reinvest them at newer, hopefully higher rates of return.