The Hidden Cost of Overtrading

In July of 2017, we wrote a piece titled “Our Favorite Holding Period is Forever.” In it, we discussed our business owner investment approach and why that naturally leads us to hold our equity investments for very long periods of time, in stark contrast to much of today’s investment industry. We stated:

Quite simply, there is no better way to compound money at attractive rates of return than the long-term ownership of successful businesses run by talented people… investors should try to identify these sorts of enterprises and people, invest in them, and let those businesses compound their investment into the future.

Since these opportunities don’t come around often, we spend much of our time preparing and waiting. There are often long periods of time with little or no trading activity in client accounts, but we always stand ready to act when opportunities appear. As Warren Buffett said, “You do things when the opportunities come along. I’ve had periods in my life when I’ve had a bundle of ideas come along, and I’ve had long dry spells. If I get an idea next week, I’ll do something. If not, I won’t do a thing.”

Our Approach is Tax Efficient

Although it isn’t frequently discussed, one substantial benefit to this approach is that it is very tax efficient for our taxable clients. As Benjamin Franklin once said, “In this world nothing can be said to be certain, except death and taxes.” We will leave the topic of death for another newsletter and instead focus on taxes.

Intuitively, most investors know that capital gains taxes negatively impact the growth of their wealth over time. However, this impact and its magnitude are typically not discussed explicitly or quantified. There is good reason for this – taxes are personal. Each person’s tax situation is different so John C. Watkins III, CFA® Vice President Equity Portfolio Managerthere is no easy, “one size fits all” formula to account for taxes. For this reason, the investment industry standard is to present portfolio returns on a pre-tax basis. This is a great starting point and allows for easy comparison against other investment strategies or funds.

Pre-tax vs. After-tax Returns

While the industry standard is pre-tax investment returns, an investor’s after-tax return is much more important. Aside from charitable giving, it is nearly impossible to spend unrealized investment gains. The purest measure of monetary wealth is how much money is left after all taxes have been paid.

Unlike most other taxes, the timing of capital gains taxes is unique in that they are entirely within the investor’s control. This is because a capital gains tax is only paid when a stock or bond is sold at a profit. Upon sale, this unrealized gain becomes a realized gain, and a tax is due.

Therefore, the main driver of the frequency and magnitude of capital gains taxes is the amount of trading activity in the investor’s portfolio, also known as portfolio turnover. Turnover is often quoted in percentages, referring to the percentage of the dollar value of the portfolio that is traded annually. For example, a $1 million portfolio with 100% turnover means that, in aggregate, there were $1 million worth of purchases or sales within the portfolio in the last 12 months.

Assuming a positive investment return over time, a higher level of trading activity triggers more capital gains taxes and results in a lower after-tax return. This phenomenon can create a sizeable, but often unnoticed, headwind to long-term investment performance.

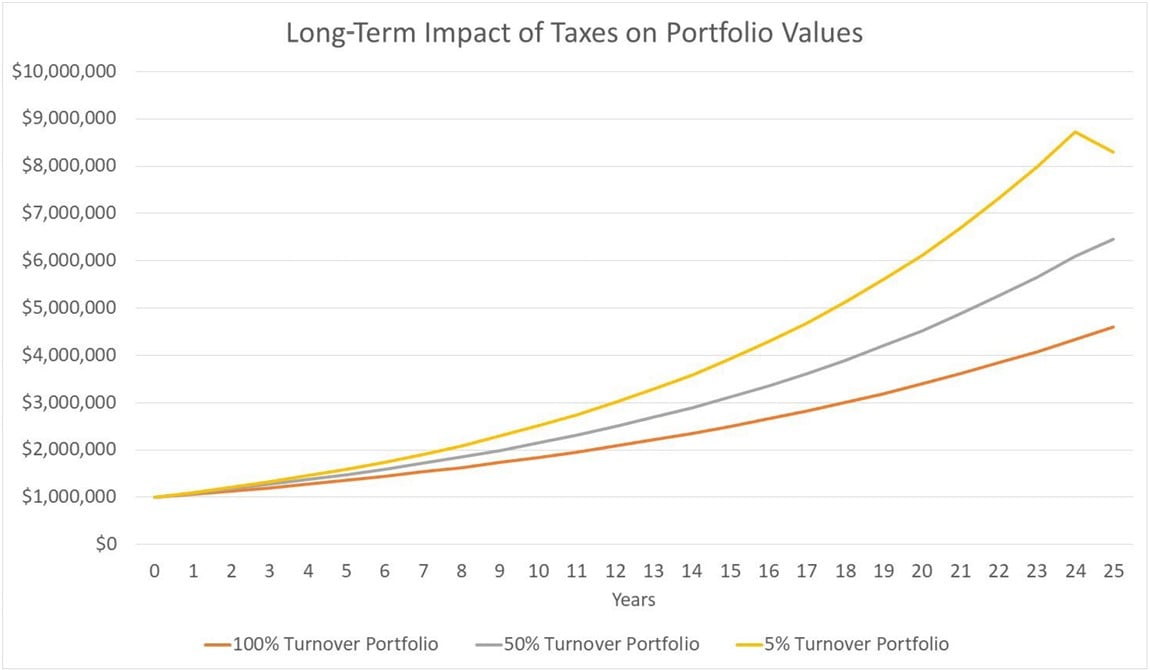

I will use a hypothetical example to illustrate. Consider three equity portfolios:

- High Turnover (100%) – A highly active, short-term trading strategy with 100% annual turnover, never holding a stock for more than one year. All capital gains are short-term in nature.

- Moderate Turnover (50%) – This portfolio typically holds stocks between six months and three years with annual turnover of 50%. There is a mix of long-term and short-term gains, with 75% long-term in nature and 25% short-term in nature.

- Low Turnover (5%) – This portfolio typically holds each of its stocks for more than 10 years with annual turnover of 5%. All capital gains are long-term in nature.

Let’s assume each portfolio starts with $1,000,000 today and achieves a pre-tax return of 10% annually over 25 years. For high income households, per the current federal tax code, short-term capital gains are taxed at 37% and long-term capital gains are taxed at 20%. For the sake of simplicity, we only focus on federal capital gains taxes. However, capital gains may also be subject to state and local taxes as well as a 3.8% federal tax surcharge for some investors. The inclusion of these would only further amplify the divergence among the three portfolios in this example. Finally, at the end of the 25-year period, any remaining unrealized gains are taxed in full at the long-term capital gains rate of 20%.

In this example, the low turnover portfolio performed the best, far outpacing the other portfolios. The values at the end of 25 years are:

- High Turnover: $4,606,081 (6.3% annualized after-tax return)

- Moderate Turnover: $6,449,918 (7.7% annualized after-tax return)

- Low Turnover: $8,298,571 (8.8% annualized after-tax return)

In this simple hypothetical example, there is only one reason for the significant difference in ending values – the timing and magnitude of capital gains tax payments. While we must acknowledge the real world is a bit more complex than this example, the underlying point remains true. The more taxes an investor pays along the way, the less money they have in the end.

Tax Leakage Stifles the Magic of Compounding

Over the short term (less than 5 years), the differences are barely noticeable, but they become clear over time. The moderate and high turnover portfolios are constantly experiencing tax leakage through trading activity that results in tax charges. Over time, these tax charges add up and have a devastating impact on the rate of return. Alternatively, the low turnover portfolio has very minimal tax leakage, allowing its unrealized gains to compound tax-deferred.

Due to these tax headwinds, highly active short-term investors are at a fundamental disadvantage compared to more patient, long-term investors. More active investment strategies must generate a higher pre-tax return simply to stay even with less active investment strategies. How much higher? In the example on page 2, the low turnover portfolio’s 10% pre-tax annual return resulted in an 8.8% after-tax annual return. To match that 8.8% annual after-tax return, the high turnover and moderate turnover portfolios must generate annual pre-tax returns of 14% and 11.4%, respectively. A tough task, indeed.

Our ultimate goal at Baird Trust is to help you compound your wealth over long periods of time while controlling for risk. We strongly believe our long-term business owner approach to investing is the best way to achieve this goal for both taxable and tax-exempt investors. But for investors with taxable accounts, our strategy’s tax efficiency is an added long-term benefit.

As always, we thank you for your relationship and continued trust you place in us as stewards of your financial assets.

To request a copy of “Our Favorite Holding Period is Forever” (2017), please email BairdTrust-Info@rwbaird.com.